Mortgages, Minus the Faff

Buying, moving, remortgaging or investing? Our award-winning service will make your journey seem simple, because it should be.

Your home may be repossessed if you do not keep up repayments on your mortgage.

Exclusive broker partner to

Working With the Brands You Trust

Why Pick Picnic?

With easy-to-use technology and 100+ experts, our award-winning service is with you every step of the way.

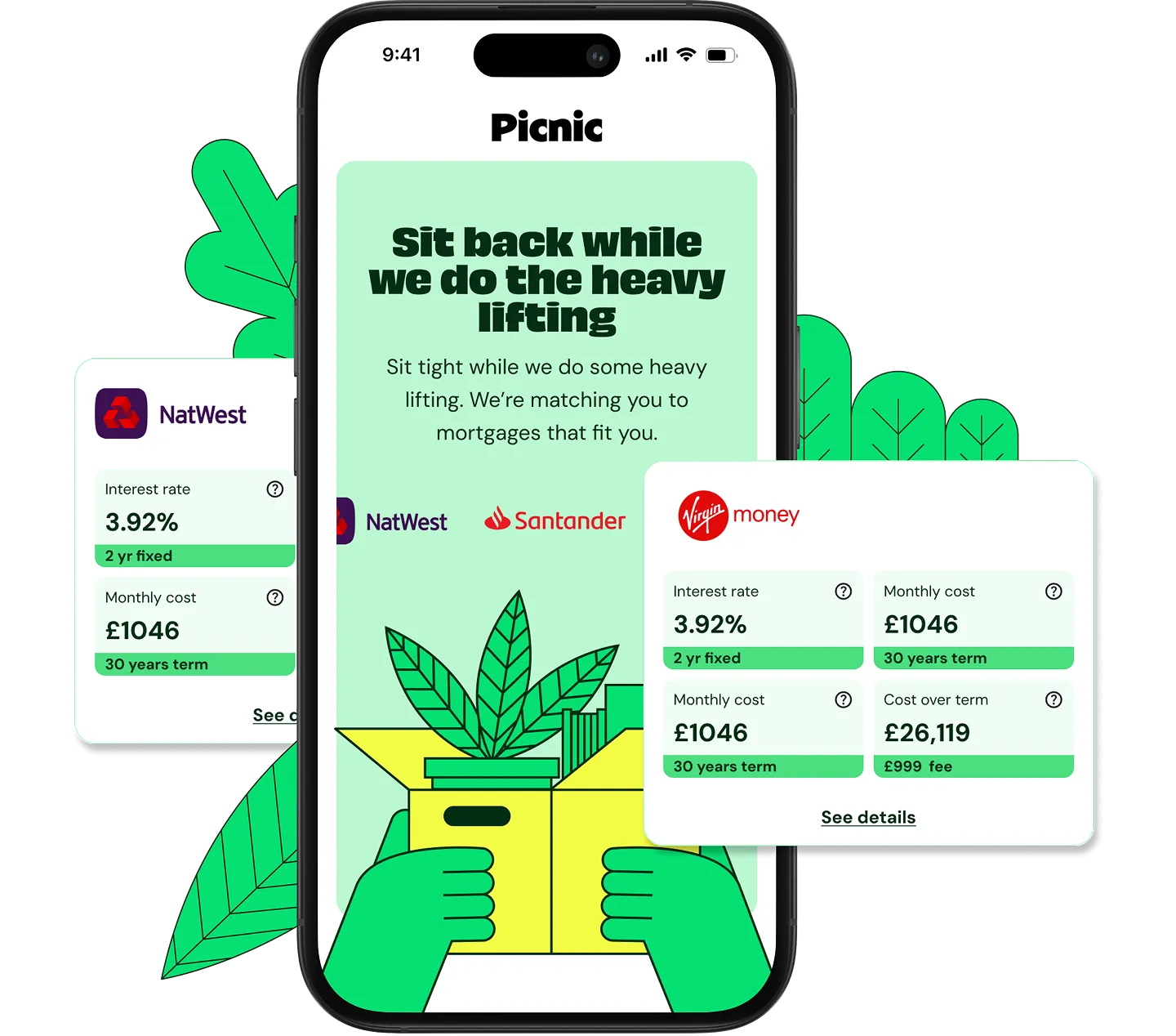

Access to 20,000+ Mortgages

We work with over 100 lenders to find you the best rate and the right mortgage, including exclusive deals you won't find online.

A Team of 100+ Experts

Award-winning advice from a team dedicated to finding the best mortgage deal for you.

Smart Tools, Easy to Use

Our innovative tech keeps you up to date at all times. All the important stuff in one smart portal.

We Work Around Your Life

Same-day appointments, evenings and weekends too — life doesn’t stop at 5.

Protection Built for You

With our free expert advice, find the cover that protects your home, income and peace of mind.

We’ve Got the Legal Side Covered

We'll provide a free conveyancing quote from one of our trusted partners.

True Agreement in Principle

A formal lender certificate — not just a number plucked from the air.

A Service You Can Trust

Brought to you by Haysto! The Specialist Mortgage Brokers who've helped thousands of people find affordable mortgage solutions to suit their needs.

The Mortgage Experts Trusted by Experian

Picnic is Experian’s exclusive mortgage partner, trusted to make mortgages simple. With access to 100+ lenders and expert support, we’ll help you find the right fit without the stress.

How Much Do You Want to Borrow?

Mortgages By Loan Amount

Created by Michael Whitehead, our Head of Content, and reviewed by Haysto co-founder, Paul Coss. Whatever mortgage you need, we've got all the bases covered so you can make the right choice.

7 mins

How to Calculate Your Mortgage Repayments

8 mins

£100,000 Mortgage

9 mins

£150,000 Mortgage

8 mins

£200,000 Mortgage

8 mins

£250,000 Mortgage

10 mins

£300,000 Mortgage

9 mins

£350,000 Mortgage

8 mins

£400,000 Mortgage

9 mins

£500,000 Mortgage

Tell Us About You

Fill out a quick 60-second form — no impact on your credit score, no endless questions.

Mortgage Match

We have access to 20,000+ products across more than 100 lenders (including exclusive deals you won’t find online) to find you the best rate and the right mortgage.

Meet Your Experts

A dedicated team handles everything. You can track your mortgage, conveyancing, and insurance progress directly from your portal.

Frequently asked questions

Mortgages 101

Whatever your circumstances, we've got all bases covered. No jargon, just real guidance to help you feel in control of your mortgage journey.

As a general rule of thumb, most mortgage lenders will offer around 4 to 4.5 times your annual income as a mortgage. This is usually the starting point. Lenders will then look further at your income and outgoings, the size of your deposit, age, and credit history to assess your overall affordability.

Everyone’s situation is different. At Picnic, our mortgage team can help you figure out exactly how much you can borrow based on your own personal circumstances. Just click the button below to make an enquiry, and we’ll help you get started.

Yes, it’s possible; these are more commonly known as 95% loan-to-value (LTV) mortgages, and most mortgage lenders offer them, albeit they’ll likely come with higher interest rates. A stable income and solid credit score will help your chances, and several mortgage schemes are available if you’re struggling to save more for a deposit.

Want to find out more? Get in touch by clicking on the button below, and one of our Mortgage Experts will contact you to discuss your situation in more detail.

With a fixed-rate mortgage, your payments stay the same for a set amount of time – no surprises, no changes. A variable-rate mortgage can fluctuate, either tracking the Bank of England base rate or moving at the lender’s discretion, meaning your payments may rise or fall over time.

So, fixed-rate mortgage deals give you peace of mind, while a variable-rate deal could work out cheaper overall, particularly if base rates are coming down (but there’s no guarantee). It’s all about what feels right for you.

If you’re unsure, why not speak to an expert? All you need to do is click the button below to make an enquiry, and a member of our mortgage team will be in touch to help you make the right decision.

A Mortgage in Principle (MIP) is a quick way to see how much a lender might let you borrow. It’s not a full mortgage offer, but it gives you a strong idea of your budget. A MIP shows both estate agents and sellers you’re a serious buyer. It can also help identify any issues early on, so you’re better prepared when applying for the real thing.

Are you ready to apply for a true Mortgage In Principle? Get in touch, and we’ll help you find one you can trust, directly from a lender, sometimes within minutes.

You’ll typically need proof of ID (passport or driving licence), proof of address (utility bills or bank statements), payslips (usually the last 3 months), bank statements (last 3–6 months), and evidence of your deposit. If you’re self-employed, you’ll need tax returns and accounts for the past 2–3 years.

To find out all you need to know about what’s needed, take a look at our guide on How to Get a Mortgage.

Yes, absolutely. Being self-employed shouldn’t mean you can’t get a mortgage; you’ll just need to show your recent tax returns and/or certified accounts rather than employment payslips as evidence of your earnings.

The key is finding the right lenders who look more favourably on self-employed applicants - and we can help you do that! To get started, click the button below to make an enquiry.

There’s no magic credit score number that automatically guarantees you’ll get a mortgage. Naturally, the better your credit score, the more options you’ll have and the better chance to qualify for the most competitive mortgage rate deals.

But, even if your credit score isn’t great, it doesn’t mean you won’t be able to get a mortgage. We help make mortgages possible for many people, even those with severe bad credit, by finding the right lenders who specialise in these situations.

Just get in touch by clicking the button below, and one of our Mortgage Experts can chat to you in more detail about your circumstances.

Yes, it’s possible. It really depends on the type of credit issue you’ve had, when it happened, and the amounts involved. Choosing the right lender can also make all the difference.

Our sister brand, Haysto, has made mortgages possible for thousands of people in similar situations by connecting them with lenders that look more favourably on applicants with adverse credit. They can help you too!

Just click on the button below to make an enquiry, and a member of our specialist mortgage team will be in touch to help you get started.